A nuanced take on fossil fuel divestment

A nuanced take on fossil fuel divestment

The important question is who ends up owning the real assets?

A common thread through many climate activism campaigns in the last decade has been a focus on fossil fuel divestment. Institutions that range from major universities to prominent pension funds and investment managers have been persuaded to divest their investment holdings from fossil fuels. The arguments for divestment seem to be accepted by many who care about climate as obvious truths, but it is worth taking a closer look at the issue in light of recent events in energy markets. Divestment looks great on paper and makes for nice public relations headlines, but I would argue there are more effective ways to use financial resources and market actions to accelerate energy transitions. Additionally, in some cases divestment might actually be counterproductive for achieving climate goals.

Fossil fuel divestment has become an article of faith among forward-thinking investment organizations. In September 2021, the Harvard endowment announced it would divest from fossil fuels after years of activist pressure, citing the threat of climate change. Harvard is just one of many organizations that have divested from fossil fuels over the last decade. Reasons for divestment have been as varied as: increasing the cost of capital for fossil fuel producers, stigmatizing fossil fuel companies, disincentivizing new fossil fuel development, and getting better returns from other sectors.

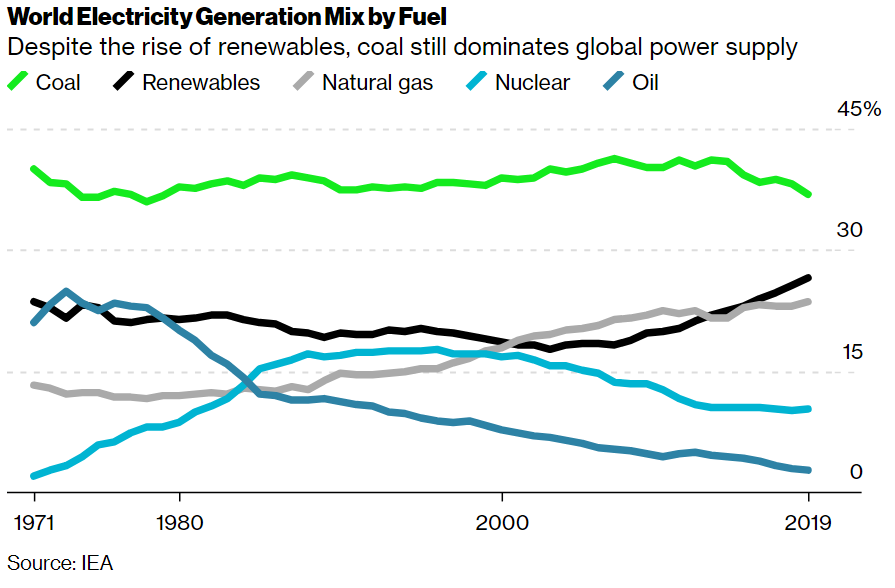

It is true that fossil fuel companies have underperformed other sectors over the previous decade. However, an energy crunch coming out of the pandemic has led to many countries tapping oil, gas, and coal reserves again, and these are still the dominant sources of energy throughout the world.

When responsible investors like university endowments and energy giants have decided not to invest in these assets, they end up with owners who are not focused on climate and environmental concerns, and eager to expand these “dirty” businesses no matter the societal cost. To quote a New Yorker editorial by William MacAskill, “As long as there are economic incentives to invest in a certain stock, there will be individuals and groups—most of whom are not under any pressure to act in a socially responsible way—willing to jump on the opportunity. These people will undo the good that socially conscious investors are trying to do.”

There’s an alternative to divestment, and that is responsible stewardship of fossil fuel resources. The activist hedge fund Engine #1 has exemplified this by taking a stake in Exxon Mobil, taking board seats, and electing directors who are aligned with a cleaner energy future for Exxon. Glencore, a giant energy conglomerate, has promised to run its coal business to closure by 2050. There are so many productive actions investors can encourage as owners of traditional energy giants, such as using oil drilling technology and expertise for geothermal energy, investing fossil fuel profits in renewable energy deployment, and creating energy transition/net zero emissions plans.

If you care about climate change, who would you rather have managing hundreds of coal mines? A university endowment that could manage a slow phase-out of the mines and perhaps repurpose their mining technology and workforce for clean energy uses, or a private equity owner unconcerned with transparency and emissions? Right now, fossil fuel divestment campaigns have left us too often with the latter type of owner, and as a financial sector, we should rethink how we use financial allocations to deal with climate change. The coal, oil, and gas resources will exist no matter who owns them, and it would be much better for these resources to have responsible and climate-conscious owners.