Welcome to the Fintech Explorer: Stripe/Paystack

Fintech Explorer Issue 1

Hello everyone, I’m Ravi Mulani, I work in Corporate Development and Strategic Finance at Credit Karma, and I’m starting a regular newsletter called the Fintech Explorer.

In this newsletter, I’ll do deep dives and explorations of different areas of the financial technology space. Please let me know if there are any topics you’d be especially interested in reading about, or have any feedback for the newsletter!

For my first issue, I’d like to cover Stripe’s acquisition of Paystack, announced on October 15th. Stripe is a large privately held American payment processor which I’ve long admired (check out this overview if you’re interested in a comprehensive introduction to the company), and Paystack offers payment tools for companies in Africa. Stripe’s acquisition of Paystack highlights the enormous financial services opportunity in Africa, Paystack’s impressive success thus far in penetrating the Nigerian payments market, and Stripe’s likely growing appetite for investments and acquisitions.

I. Market Opportunity in Africa

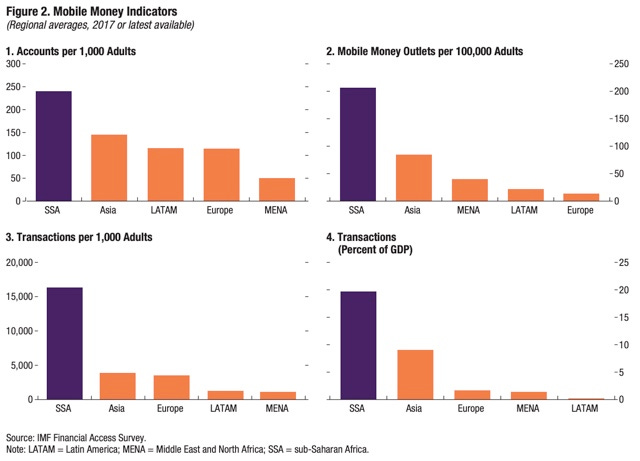

The market opportunity in Africa for financial technology companies is absolutely enormous. Per an IMF report in 2019, “Sub-Saharan Africa leads the world in mobile money accounts per capita, mobile money outlets, and volume of mobile money transactions.” M-Pesa, one of the first “mobile money” services, was first launched in Kenya by Vodafone and Safaricom. Here are a few charts showing the depth of penetration of “mobile money” services in Sub-Saharan Africa:

Similar to developments in much of Asia, Africa has leapfrogged building an American-style financial system with tons of physical branches and infrastructure and moved directly to mobile and digital financial services given the timing of economic development on the continent.

That being said, there are some dynamics of e-commerce growth in Africa similar to that in America and elsewhere. In an interview with McKinsey, the CEO of Jumia notes that “there are a lot of consumers who are not necessarily in the big urban areas,” because e-commerce offers them more choice, variety, and convenience than the in-person shopping options they have in their home regions. We’ve seen a similar development in Amazon’s penetration of rural America.

As more Africans get online and get shopping online, and the continent as a whole continues to generate new businesses and compounding wealth, it’s a great time to build a financial services business facilitating online commerce in Africa, and Paystack has executed well thus far in Nigeria.

II. Paystack’s Success

Paystack has had remarkable success in just a few years since being founded in January 2016. It was the first Nigerian company accepted to Y Combinator, and in just under five years it has grown to process over 50% of the online transactions in Nigeria. Similar to Stripe, Paystack provides APIs to create a seamless payment processing experience for Nigerian companies and institutions. Customers already include Domino’s, the Lagos Internal Revenue Service, AXA, and various major Nigerian brands. Over 60,000 businesses use Paystack for their payment processing needs. Indeed, Paystack has a “wall of love” on its website with customer testimonials that highlight the product’s versatility and efficacy.

Given the current and potential size and depth of the African online payments market, Paystack is only scratching the surface of what they might be able to achieve in the coming years. They’ve launched a pilot in South Africa already, and as discussed, countries across Africa, including Ghana, Kenya, Morocco, and South Africa, to name a few, already have impressive levels of internet penetration and are promising potential markets for Paystack to explore.

Paystack will certainly face stiff competition in the African payments market. Most notably, Flutterwave, an SF-based payments processor with operations in multiple African countries, raised a sizable Series B in January and is also a major player in Nigeria. However, this is where Stripe’s support will be useful; Stripe’s financial resources, existing customer relationships, global reach, and payments expertise could be critical to Paystack’s success in expanding across African markets. Additionally, the African market has the potential to be so large that similar to the U.S. market, there will be space for multiple payments winners in the region.

III. Stripe’s Likely Growing Appetite for Acquisitions and Investments

Stripe is likely sitting on a substantial chest of cash from numerous recent funding rounds, and given its most recent public funding valuation was $36 billion, its stock is a good currency for potential acquisitions. Until now, Stripe’s activity in this space has been primarily making investments and acquihires.

In recent years, Stripe has made investments in numerous early-stage companies, including a Series A in Paystack, a Series A in Fast (a checkout tool), a Seed Investment in Pulley (an equity management tool), and PayMongo, which facilitates internet payments in the Philippines. As seen in the case of Paystack, an early investment can often help a company such as Stripe glean information and access that allow it to make earlier and savvy judgments on potential acquisitions.

I expect Stripe’s acquisition appetite to increase as it seeks to grow a truly global payments platform and expand into various aspects of online financial services. Stripe’s mission to increase the GDP of the internet can encompass a very broad array of financial services, and I’m looking forward to seeing how they grow through investing and M&A going forward.